By Lyndsey Stram, Regional Economist; Lecia Parks Langston, Senior Economist

“You have power over your mind — not outside events. Realize

this, and you will find strength.” Marcus Aurelius

In the wake of the COVID-19 pandemic, businesses lost revenues and workers lost jobs. But because of the time it takes to collect and collate data, economists have been left without much information to quantify the economic impacts at the local level.

But there is one ray of data illumination. Claims for unemployment benefits are promptly available and provide information about a large cross section of the economy. This post will outline what light unemployment claims data sheds on the state of the Mountainland Region’s economy.

While not all workers are protected by unemployment insurance laws, roughly 95% of jobs are covered. This makes claims data an exceptional source of information about the economy. Not included under unemployment insurance laws are most self-employed workers, about half of agricultural employment, unpaid family workers, railroad personnel (covered separately) and many nonprofit organizations (such as churches). Also, some out-of-work employees may not have worked a sufficient work history to qualify for unemployment insurance benefits, but may file anyway.

Fortunately, in this time of economic distress, the social safety nets of the unemployment insurance program, special national COVID-19 funding and social programs are working together to keep workers’ income and well-being stable.

Unemployment claimants and the unemployed; they aren’t the same

Also, keep in mind that, in addition to individuals drawing unemployment benefits, the unemployment rate includes those entering and re-entering the workforce and non-covered groups without current employment. This means the number of “unemployed” will be greater than the number of claimants. In “normal” times, only about 40% of the “unemployed” are claiming benefits.

The generally reported unemployment rate also has a work-search requirement. If you haven’t made any minimal attempts to find work, you aren’t counted as “unemployed.”

Watch this Space

While this analysis won’t be updated on a regular basis, new data will be added to the data visualization on a weekly basis allowing readers to check back for the latest information.

An Unprecedented Event

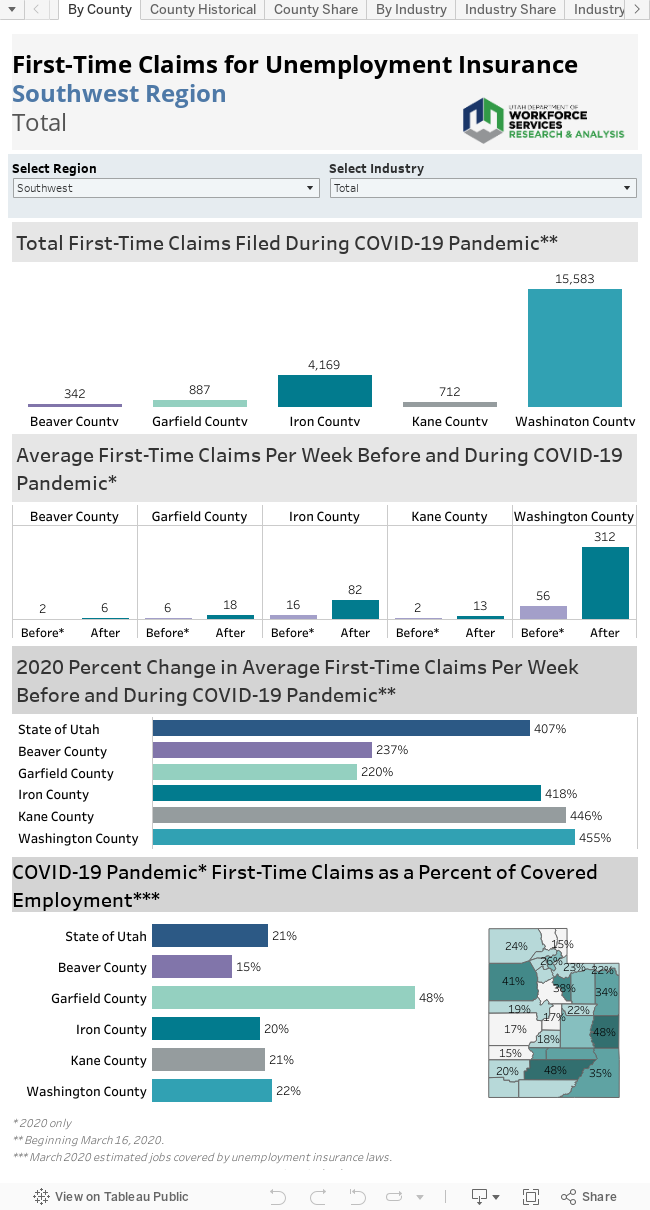

Not surprisingly, first-time claims for unemployment benefits soared in Utah and across the nation as the pandemic swept across the country. Week 12 (beginning March 16) marks the beginning of the unprecedented surge in claims. Claims in the Mountainland region peaked in week 14 and have been decreasing since. On a positive note, while new claims for unemployment insurance have skyrocketed in Utah, the state currently shows one of the lowest claims rates in the nation.

For most Mountainland counties, initial claims peaked in the second week of the pandemic and have since tapered downward. During the peak week 14, initial claims filed totaled 6,474 in the region. As of week 19, the level of claims as decreased significantly. However, for many counties, the level of claims is still well above normal levels and even above levels seen during the Great Recession.

Who took the hardest hit?

Counties that have a large share of their employment dependent on tourism have felt the greatest impact and employment shocks. This is particularly true for Summit County, the site of many of the first cases of COVID-19 in Utah. Summit County’s economy is largely dependent on its world-class ski resorts and the 2019-2020 ski season was suspended early to curtail the outbreak.

Wasatch County is also largely dependent on tourism and this is where the largest share of claims as a percentage of covered employment occurred in the region: 21%. This is the second highest share in the state.

Tourism and COVID-19

Especially in the early stages of the pandemic, this is a story of tourism-dependent industries. Almost 15% of the COVID-19-related initial claims filed in Utah’s Mountainland region represented workers previously employed in accommodations and food services. In addition, the true effect of the pandemic on this industry is masked by a large number of claims classified as industry “unknown” in the early days of the claims flood. Undoubtedly, many of these claims would rightfully be classified in accommodations/food services if the appropriate information were available.

Other high-claims industries included retail trade, healthcare/social assistance (reflecting the cessation of elective procedures and visits) and administrative support/waste management/remediation (the home to temporary employment agencies). Many of these high-claim industries reflect their high share of total employment. In addition, they often serve the public face to face, or face damage due to the decline in demand for travel.

The High and the Low

Although accommodations/food services has generated the largest number of claims in Mountainland, initial claims in the COVID-19 time period, in percentage terms, other industries have suffered comparably. For example, administrative support/waste management/remediation has also seen 16% of its covered workforce file for claims.

Surprisingly, construction, which usually accounts for a larger percentage of claims, has only seen 4% of its workers file since the COVID-19 pandemic hit. The relative ease of social distancing and the nature of the work has allowed construction to hold on to its workforce.

Utilities, public administration and education have also been able to keep a higher portion of their workforce employed.

County by County

Juab County

• Prior to the COVID-19 pandemic, the average number of weekly first-time claims in Juab County was five. This has since increased by 513% to 31 average weekly claims.

• Juab County has seen the smallest rise in claims and the lowest percent of covered workforce filing for claims in the region.

• Three sectors account for nearly 50% of the claims filed in Juab County: accommodation/food service, healthcare/social assistance, and manufacturing.

• Juab County accounted for 2% of Mountainland’s new claims prior to the pandemic, but only 1% since.

Summit County

• Prior to the COVID-19 pandemic, the average number of weekly first-time claims in Summit County was 15. This has since increased by 3,716% to 562, the largest increase in the region.

• Summit County suffered from the start as the site for some of the earliest cases of COVID-19 in Utah and with its high dependence on tourism, especially during the early spring and summer months.

• Unsurprisingly, a huge share of claims came from the accommodations/food services sector. This accounts for at least 32% of the total claims in Summit County (and likely many of the unknown industry claims).

• Other hard-hit industries in Summit County include arts/entertainment/recreation and retail trade.

• Summit County accounted for 6% of Mountainland’s new claims prior to the pandemic and 16% during.

Utah County

• Prior to the COVID-19 pandemic, the average number of weekly first-time claims in Utah County was 197. This has since increased to 562 claims, an increase of 1,281%.

• Utah County accounts for the largest employment share in the Mountainland region and also has the most diverse economy compared to the other counties. This diversity helps the economy weather employment shocks being experienced now.

• Healthcare/social assistance, retail trade and administrative support/waste management/remediation account for the majority of claims filed in Utah County.

• Utah County accounted for 87% of the new claims in the region prior to the pandemic, and only 76% during.

Wasatch County

• Prior to the COVID-19 pandemic, the average number of weekly first-time claims in Wasatch County was 11. This has increased by 2,543% to 279 average first-time weekly claims.

• A significant 21% of the covered workforce in Wasatch County has filed a claim for unemployment. This is the second highest share in the state.

• Wasatch County’s economy is largely dependent on tourism, making it a hard-hit area. Roughly 59% of the arts/entertainment/recreation workforce has filed claims, as well as 46% of the accommodation/food service sector.

• Wasatch County accounted for 5% of the new claims in the region prior to the pandemid, and 8% during.

But there is one ray of data illumination. Claims for unemployment benefits are promptly available and provide information about a large cross section of the economy. This post will outline what light unemployment claims data sheds on the state of the Mountainland Region’s economy.

While not all workers are protected by unemployment insurance laws, roughly 95% of jobs are covered. This makes claims data an exceptional source of information about the economy. Not included under unemployment insurance laws are most self-employed workers, about half of agricultural employment, unpaid family workers, railroad personnel (covered separately) and many nonprofit organizations (such as churches). Also, some out-of-work employees may not have worked a sufficient work history to qualify for unemployment insurance benefits, but may file anyway.

Fortunately, in this time of economic distress, the social safety nets of the unemployment insurance program, special national COVID-19 funding and social programs are working together to keep workers’ income and well-being stable.

Unemployment claimants and the unemployed; they aren’t the same

Also, keep in mind that, in addition to individuals drawing unemployment benefits, the unemployment rate includes those entering and re-entering the workforce and non-covered groups without current employment. This means the number of “unemployed” will be greater than the number of claimants. In “normal” times, only about 40% of the “unemployed” are claiming benefits.

The generally reported unemployment rate also has a work-search requirement. If you haven’t made any minimal attempts to find work, you aren’t counted as “unemployed.”

Watch this Space

While this analysis won’t be updated on a regular basis, new data will be added to the data visualization on a weekly basis allowing readers to check back for the latest information.

An Unprecedented Event

Not surprisingly, first-time claims for unemployment benefits soared in Utah and across the nation as the pandemic swept across the country. Week 12 (beginning March 16) marks the beginning of the unprecedented surge in claims. Claims in the Mountainland region peaked in week 14 and have been decreasing since. On a positive note, while new claims for unemployment insurance have skyrocketed in Utah, the state currently shows one of the lowest claims rates in the nation.

For most Mountainland counties, initial claims peaked in the second week of the pandemic and have since tapered downward. During the peak week 14, initial claims filed totaled 6,474 in the region. As of week 19, the level of claims as decreased significantly. However, for many counties, the level of claims is still well above normal levels and even above levels seen during the Great Recession.

Who took the hardest hit?

Counties that have a large share of their employment dependent on tourism have felt the greatest impact and employment shocks. This is particularly true for Summit County, the site of many of the first cases of COVID-19 in Utah. Summit County’s economy is largely dependent on its world-class ski resorts and the 2019-2020 ski season was suspended early to curtail the outbreak.

Wasatch County is also largely dependent on tourism and this is where the largest share of claims as a percentage of covered employment occurred in the region: 21%. This is the second highest share in the state.

Tourism and COVID-19

Especially in the early stages of the pandemic, this is a story of tourism-dependent industries. Almost 15% of the COVID-19-related initial claims filed in Utah’s Mountainland region represented workers previously employed in accommodations and food services. In addition, the true effect of the pandemic on this industry is masked by a large number of claims classified as industry “unknown” in the early days of the claims flood. Undoubtedly, many of these claims would rightfully be classified in accommodations/food services if the appropriate information were available.

Other high-claims industries included retail trade, healthcare/social assistance (reflecting the cessation of elective procedures and visits) and administrative support/waste management/remediation (the home to temporary employment agencies). Many of these high-claim industries reflect their high share of total employment. In addition, they often serve the public face to face, or face damage due to the decline in demand for travel.

The High and the Low

Although accommodations/food services has generated the largest number of claims in Mountainland, initial claims in the COVID-19 time period, in percentage terms, other industries have suffered comparably. For example, administrative support/waste management/remediation has also seen 16% of its covered workforce file for claims.

Surprisingly, construction, which usually accounts for a larger percentage of claims, has only seen 4% of its workers file since the COVID-19 pandemic hit. The relative ease of social distancing and the nature of the work has allowed construction to hold on to its workforce.

Utilities, public administration and education have also been able to keep a higher portion of their workforce employed.

County by County

Juab County

• Prior to the COVID-19 pandemic, the average number of weekly first-time claims in Juab County was five. This has since increased by 513% to 31 average weekly claims.

• Juab County has seen the smallest rise in claims and the lowest percent of covered workforce filing for claims in the region.

• Three sectors account for nearly 50% of the claims filed in Juab County: accommodation/food service, healthcare/social assistance, and manufacturing.

• Juab County accounted for 2% of Mountainland’s new claims prior to the pandemic, but only 1% since.

Summit County

• Prior to the COVID-19 pandemic, the average number of weekly first-time claims in Summit County was 15. This has since increased by 3,716% to 562, the largest increase in the region.

• Summit County suffered from the start as the site for some of the earliest cases of COVID-19 in Utah and with its high dependence on tourism, especially during the early spring and summer months.

• Unsurprisingly, a huge share of claims came from the accommodations/food services sector. This accounts for at least 32% of the total claims in Summit County (and likely many of the unknown industry claims).

• Other hard-hit industries in Summit County include arts/entertainment/recreation and retail trade.

• Summit County accounted for 6% of Mountainland’s new claims prior to the pandemic and 16% during.

Utah County

• Prior to the COVID-19 pandemic, the average number of weekly first-time claims in Utah County was 197. This has since increased to 562 claims, an increase of 1,281%.

• Utah County accounts for the largest employment share in the Mountainland region and also has the most diverse economy compared to the other counties. This diversity helps the economy weather employment shocks being experienced now.

• Healthcare/social assistance, retail trade and administrative support/waste management/remediation account for the majority of claims filed in Utah County.

• Utah County accounted for 87% of the new claims in the region prior to the pandemic, and only 76% during.

Wasatch County

• Prior to the COVID-19 pandemic, the average number of weekly first-time claims in Wasatch County was 11. This has increased by 2,543% to 279 average first-time weekly claims.

• A significant 21% of the covered workforce in Wasatch County has filed a claim for unemployment. This is the second highest share in the state.

• Wasatch County’s economy is largely dependent on tourism, making it a hard-hit area. Roughly 59% of the arts/entertainment/recreation workforce has filed claims, as well as 46% of the accommodation/food service sector.

• Wasatch County accounted for 5% of the new claims in the region prior to the pandemid, and 8% during.