Consumer spending makes up around 68 percent of the nation’s

gross domestic product. Consumer spending is individuals and families

purchasing groceries, clothing, recreation, stocks, insurance, education and much

more. The transactions cover a broad swath of economic activity.

Much of the nation’s consumer spending is captured via

retail trade. A useful retail trade definition

is “the re-sale (sale without

transformation) of new and used goods to the general public, for personal or

household consumption or utilization.” Not all consumer spending is captured through

retail trade transactions, but majority large share is.

Whereas in the past nearly all retail transactions were done

through traditional brick-and-mortar stores, now a significant and growing

segment is diverted to internet sales. The consumer shops online and FedEx (or

like) delivers the product. One can see that the number of brick-and-mortar

stores and the level of local sales across the country are being endangered by this

economic evolution.

The brick-and-mortar reduction is beginning to show its economic

presence in the United States employment numbers. While the U.S. economy is

finally expanding at a healthy pace this side of the Great Recession, one of

the few industries not rising with this tide is retail trade. While overall

retail sales are increasing, employment is not.

Traditionally, as a population increases, retail trade

employment grows simultaneously, since population growth and consumer spending volume

is an integrated dynamic. If studied deeply, a certain ratio of retail trade employment

growth spawned from population growth would emerge.

Before the internet, the

vast majority of all consumer sales occurred in the immediate community or

region. But now, the internet is diverting these sales away from the local

community — and with internet sales growing, its market share will increase.

We do not yet know how much brick-and-mortar erosion will eventually

occur. And will such a phenomenon hit some areas more than others (e.g., urban

vs. rural, or local vs. tourist spending)? These are touch points that

economists will be watching as this internet sales phenomenon continues to grow

within the national and Utah economies.

In light of this change, in this quarter’s Local Insights we

are profiling retail trade employment throughout Utah’s local regions. This can

offer a profile of where retail trade is now in a local economy, and possibly

how much of the sector could become vulnerable to the internet-sales

phenomenon.

All regions can be viewed through the Local Insights web

portal. The following is a retail trade profile for the Mountainland region:

Measuring

Retail – NAICS Codes

In order to explore

the relationship between internet and brick-and-mortar retail we need to look

at data grouped through the North

American Industry Classification System (NAICS), which “is the standard

used by Federal statistical agencies in classifying business establishments.” Stated

simply, the NAICS groups businesses together based upon what they do.

Hierarchical in

nature, the NAICS begins with a broad categorization and narrows its focus at

subsector levels. As an example, the educational services sector includes all

institutions focused on providing instruction and training. At the subsector

levels, that focus is narrowed so that data from elementary schools, colleges

and trade institutions are separated.

In the case of

retail, a broad sector known as retail trade includes several underlying categories

such as: motor vehicle sales, furniture stores, electronics stores, building

material stores, grocery stores, pharmacies, gas stations, clothing stores and

department stores, among others.

Then there is the

relatively new and emerging part of the retail trade sphere — non-store

retailers. These are establishments that sell products primarily on the internet

or through direct selling. Examples include Amazon, Overstock.com, Young Living

and dōTERRA. These types of retailers have grown rapidly in the past 15 years

and their presence is reshaping the retail trade landscape. We will look at

this subsector in a later section.

Retail in

the Mountainland Region

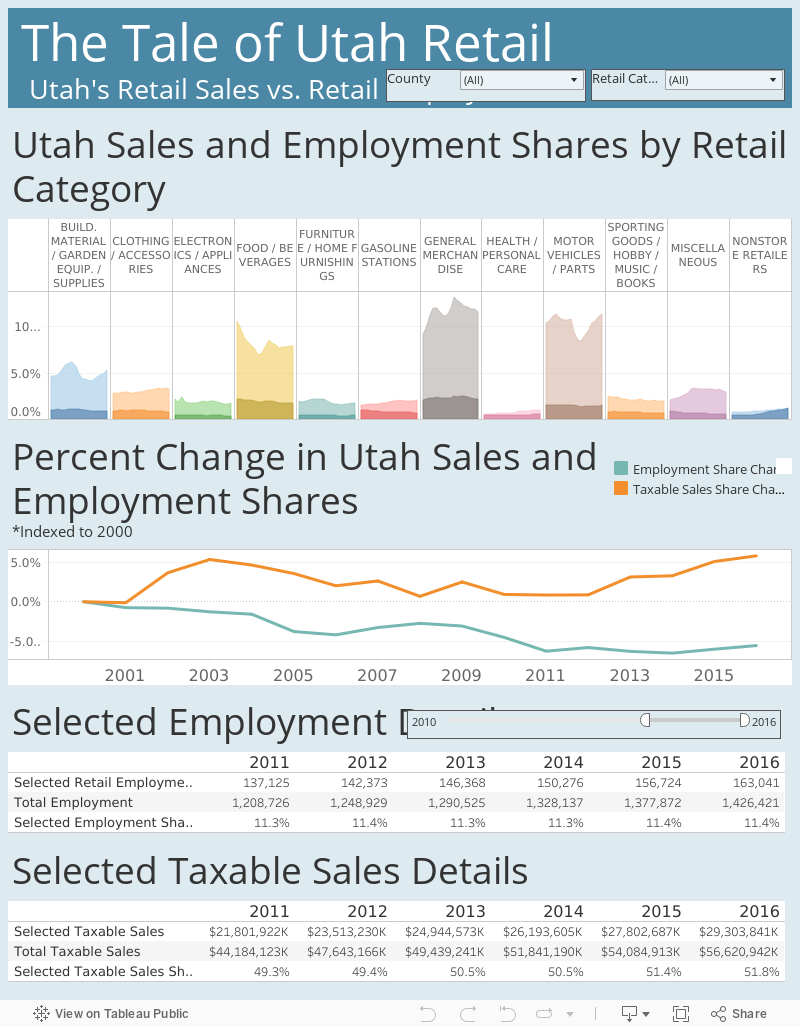

In 2016, retail trade accounted for 12.8 percent of

employment in the four Mountainland counties making it one of the largest

industries with nearly 35,000 jobs. The three largest retail subsectors in the area

are general merchandise stores, food and beverage stores, and motor vehicle and

part dealers. These three account for 41 percent of retail employment in the

area are responsible for nearly a third of all taxable sales in the four

counties.

This and other data are represented in the visual below, which

illustrates trends in retail employment and taxable sales between 2000 and

2016. From this visual we see that retails’ share of employment has declined in

recent years. On the surface, this may indicate that the internet is replacing

“vulnerable” brick-and-mortar jobs with employment in electronic shopping

related industries.

While many of these online retail jobs are counted in

non-store retailers, some worksites may be placed in other industries like

transportation and warehousing. As an example, despite their online storefront,

the distribution center for Backcountry.com in West Valley City is classified

as a warehousing establishment. This structural difference between online and

traditional retail may account for some of the employment share reduction, but

to what extent is it driven by the internet supplanting vulnerable retail

locations?

Infrastructure,

Perishability and Behavior – Identifying Vulnerable Retail Sectors

One way to identify potential vulnerabilities in

brick-and-mortar retail employment is to explore trends in e-commerce sales

relative to total retail sales. While this data is unavailable at the region

and state level it is provided for the U.S. Despite the lack of geographical

specificity in the data, it captures trends and relationships in an industry

where borders are disappearing due to the growing accessibility of the

internet.

In order to identify vulnerable employment, we will identify

subsectors which have been impacted most by online shopping. We can do this by

looking at internet sales penetration within retail, which is the share of

online sales for a particular subsector, and comparing it to employment in

Utah, Summit, Juab and Wasatch counties. For this portion of the analysis, we

will exclude non-store retailers and look at “traditional” brick-and-mortar

retail groupings and their online sales.

Mountainland Employment

vs. Internet Sales Penetration

Source: Census Bureau E-Stats

This graph illustrates four main points about the

connection/competition between brick-and-mortar and online stores.

First, not all industries are currently well-suited for

internet sales and may lack the infrastructure required. This is seen primarily

in the low online sales levels in general merchandise (one-stop shopping) and

food/beverage (grocery) stores. While the idea of having all your groceries and

toiletries shipped is appealing, the infrastructure to transfer these

perishable goods to a large amount of households in a timely manner does not

yet exist. Conversely, the electronics subsector appears to be much better

suited for online sales. Perhaps it is because individuals purchasing

technology are comfortable with using technology to purchase it.

The second insight we can glean from the graph is the impact

of product on labor needs. A food and beverage store will require more

employees to care for perishable goods relative to a furniture store where

products rotate only a few times annually. Books, clothing and electronics are

also examples of products requiring less labor to maintain. Therefore, the less

maintenance an inventory requires, the higher the likelihood that it will

transition to online sales.

Third, the motor vehicle and part dealer subsector is

unique. While perishability of goods can explain the need for higher employment

levels in the grocery groupings, a car doesn’t expire the way a gallon of milk

does. While some of the higher employment in motor vehicles may be explained by

a lack of infrastructure in shipping cars purchased online, it may be more of a

behavioral driver. According to a 2015 Autotrader

survey, 88 percent of consumers said they wouldn’t buy a car before a test

drive.

These first three points illustrate that infrastructure,

perishability and behavior all influence the degree to which certain retail

groups sell online.

The final point is the negative relationship between

internet sales penetration and employment. In general, higher levels of internet

sales penetration are correlated to low regional employment in that industry.

This confirms visually that jobs gained with online retailers reduce employment

among traditional retail.

What About

Non-Store Retailers?

As mentioned previously, the graph above excluded non-store

retailers. In the Mountainland area, this subsector employs more than 6,200

individuals, making it the largest retail category. Of these jobs, over 4,000

are found in the direct selling category which encompasses in-house sales,

truck or wagon sales and portable stalls. With the rise of essential oil

companies like Young Living and dōTERRA,

among other multi-leveling marking (MLM) companies, Utah County has become a

bastion of this type of retail activity. Since 2000, employment in this subsector

has grown by 595 percent (mostly since 2007) and taxable sales have grown by 63

percent. So why are non-store taxable sales gaining at a slower pace than

employment?

In the case of direct selling, many MLM workers are

contracted labor, in other words they operate as self-employed workers. This

means their taxable sales will not be captured in a retail NAICS code, and

cannot be tracked. In online sales, taxes are collected by the state of the

purchaser, and then, only if the seller has a physical presence in that state. This

means that when Overstock.com sells a rug to someone outside of Utah, there is

money coming into Utah (in terms of the jobs that the sale supports), but there

is no sales tax coming in to Utah. The only non-store sales taxes captured in

Utah are Utah consumers purchasing goods from retailers with a presence in

Utah. Since a large share of sales by local online retailers are to customers

in other states, it means that sales tax revenue lags compared to employment

growth in the industry.

Direct sales (MLM) and companies like Overstock.com

illustrate the difficulties in quantifying the impact of non-store retailers on

brick-and-mortar locations. When Utah residents purchase tax-free goods from a

non-store retailer like Amazon or from a direct sales company, establishing a

relationship between non-store and traditional retail is challenging.

Perhaps the state’s recent agreement with Amazon will be

helpful in unraveling part of this puzzle. Amazon recently established a nexus

with the state of Utah and therefore became obligated to collect sales taxes. Amazon

reportedly captured 33 percent of all US online purchases in 2015, according to

the magazine Internet Retailer, up from 25 percent in 2012. Conversely, direct

selling firms will continue to create challenges as long as the current data

methodology and MLM business model is preserved.